Chief executive officer's report

It gives me pleasure to report on another very successful year for the Assore group.

The financial results of the group are largely dependent on the level of global economic growth as the majority of commodities produced are used in the production of crude and stainless steels, the consumption of which is directly related to global capital spend.

In addition, group results are significantly affected by US dollar commodity prices and prevailing exchange rates which are risks that are generally beyond the control of management.

Safety

Dwarsrivier improved its lost-time injury frequency rate (LTIFR) to 0,17 for FY19 from 0,19 in FY18. The mine achieved five million fatality-free shifts in March 2019 and its safety performance contributed significantly to an improvement of the LTIFR of the operations controlled by Assore to 0,22 for FY19 from 0,27 in FY18.

The operations of Assmang, which are jointly controlled by Assore and ARM, achieved a combined LTIFR of 0,19 for FY19, representing a deterioration from the level recorded in FY18 of 0,13. However, its operations continue to maintain and achieve exceptional safety records. Khumani Iron Ore Mine achieved the best LTIFR in its operational history of 0,08, while Beeshoek Iron Ore Mine achieved four million fatality-free shifts in January 2019. In the Manganese division, the Black Rock Mines achieved seven million fatality-free shifts in February 2019, with the Cato Ridge smelters completing a second consecutive year without a lost-time injury.

The group remains committed to pursuing sustainable improvement in its overall safety performance.

Markets

The group's major markets are located in the Far East, India, Europe, North America and South Africa. Although the group's sales for iron and manganese products are reasonably diversified, the Chinese market remains the dominant destination for the group's products, especially for chrome ore. Diversification has been achieved through the establishment of long-term supply relationships, both directly and through agents. The group continues to develop other markets using its existing industry knowledge while anticipating future market developments.

World crude steel production grew by 4,5% in the 2018 calendar year (CY18), led by Chinese demand for crude steel which remained firm due to continued economic stimulus. Production in China is expected to grow by 5,7% in the 2019 calendar year (CY19). China produces more than half of the world's supply of crude steel and continues to report high levels of crude steel production, reaching 89 million tons in May 2019, which represented an all-time monthly record. The increases in global steel output drove good levels of demand for ores, with increased prices for iron ore and stable prices for manganese ore. Sustained, tight environmental controls continue to drive demand for the group's high-grade products.

The trade conflict between the USA and China has had a negative impact on consumer and business confidence and resulted in a lower than expected demand for stainless steel. As a result, prices for stainless steel and subsequently chrome ore prices weakened throughout FY19. This pricing weakness occurred despite an increase in world production of stainless steel for CY18, which increased by 5,4% from the 2017 calendar year (CY17).

Earnings

The favourable market conditions experienced in the period enabled the group to sell increased volumes of manganese ore and alloys and maintain the volumes of chrome ore sold in FY18.

The average SA rand/US dollar (ZAR/USD) exchange rate for FY19 was R14,12, 10% weaker than the level that prevailed during FY18. The weaker exchange rate, higher iron ore prices, elevated although steadily declining manganese ore prices, and higher sales volumes of manganese ore, resulted in a notable increase in headline earnings (25%) with contributions to headline earnings/(loss) by commodity as follows:

| FY19 R million |

FY18 R million |

|||

| Iron ore | 3 885 | 2 004 | ||

| Manganese | 2 021 | 2 211 | ||

| Chrome | 514 | 845 | ||

| Other group transactions | (38) | 49 | ||

| Per consolidated income statement | 6 382 | 5 109 |

The group, through its wholly owned subsidiary Ore & Metal, is the sole marketing and distribution agent for all the group's products, including those of Assmang.

The sales volumes for Assmang (iron ore and manganese) and Dwarsrivier (chrome ore) for the current and previous years were as follows:

| FY19 Metric ton ’000 |

FY18 Metric ton ’000 |

% (decrease)/ increase |

|||

| Iron ore | 17 543 | 17 874 | (2) | ||

| Manganese ore* | 3 434 | 3 177 | 8 | ||

| Manganese alloys | 398 | 378 | 5 | ||

| Chrome ore | 1 556 | 1 557 | – |

* Excludes intragroup sales to alloy plants.

Iron ore

The increase in attributable profit for FY19 is due to the increase in prices and the weaker ZAR/USD exchange rate over the financial year. The average market price for iron ore increased over FY19 from USD69 per ton (62% iron content, "fines" grade, delivered in China) to USD80 per ton. At the end of FY19, the iron ore price level reached USD118 per ton, a level last recorded in 2014. A tragic tailings dam failure in Brazil, as well as weather disruptions in northern Brazil and Western Australia, resulted in reduced seaborne supply of iron ore. Furthermore, improved levels of demand for steel in China, mainly as a result of economic stimulus measures, changed what was anticipated to be an oversupplied market into an undersupplied market.

The strong demand for the group's product, combined with an increase of approximately 60% in the average level of the "lumpy" premium, to USD21 for FY19 (FY18: USD13) per ton, contributed to the increase in iron ore revenue of 39%. Sales volumes for FY19 were slightly lower (2%) than those for FY18, due to logistical difficulties encountered on the export rail line to Saldanha and requirements to balance inventories on site and at port. Production volumes decreased by 4% due to water supply challenges experienced at Khumani Mine.

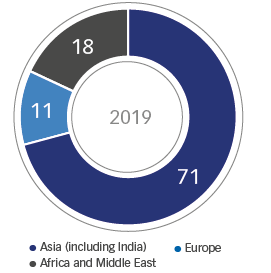

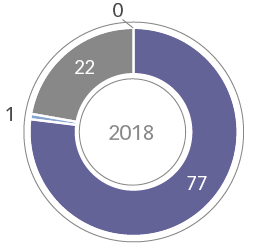

Assmang's sales strategy for iron ore is to supply those markets that show a higher degree of stability, increasing sales in the higher return markets and attempting to diversify country risk. China remains the group's largest market. Limited progress was made in concluding a higher proportion of sales to other countries during FY19. On a per-region basis, the sales volumes for the year and FY18 are illustrated as follows:

| Sale of iron ore on a per-region basis (%) | |

|

|

Capital expenditure in the Iron Ore division amounted to R2,1 billion, an increase of 18% on FY18, relating mostly to the replacement of additional mining fleet machinery.

Manganese ore and alloys

The growth in steel production ensured that demand for manganese ores remained firm throughout FY19, resulting in stable index prices, despite some weakness in Chinese ferroalloy prices towards the end of FY19.

The manganese ore market was characterised by significant changes in the Chinese ferroalloy industry which saw silico-manganese production increase by 30% in CY18. This was driven by an increase in the unit consumption of silico-manganese due to changes in the Chinese rebar steel quality standards implemented in early 2018, requiring an increase of manganese content in rebar from 8kg/ton to approximately 11kg/ton. On the supply side, domestic Chinese manganese ore production continued to decline.

The FY19 average index price for the high-grade "lumpy" ore (44% manganese content) was USD6,68 per dry metric ton unit (dmtu), delivered (CIF) in China (FY18: USD6,88 per dmtu), while the average medium-grade "lumpy" ore price index (37% manganese content) for FY19 was USD5,55 per dmtu, free on board (FOB) from South Africa (FY18: USD5,59 per dmtu).

The stable prices together with the 8% increase in sales volumes and the weak ZAR/USD exchange rate resulted in the increased earnings from manganese ore. Production volumes decreased by 8% due to the five-and-a-half months shut at the Gloria Mine for its modernisation and optimisation project.

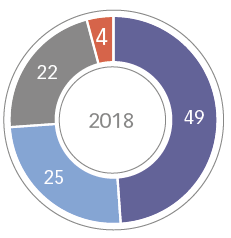

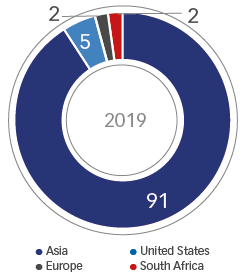

The distribution of manganese ore sales on a per-region basis for the current and previous financial year is illustrated as follows:

| Sale of manganese ore on a per-region basis (%) | |

|

|

Despite the strong steel production, the manganese alloy market remained over-supplied during the reporting period. This resulted in continued price weakness and poor profitability for ferroalloy producers, with greater pressure on non-integrated producers.

The average index price for the USA and Europe for the FY19 for high-carbon ferromanganese was USD1,245 per ton delivered (including duties) (DDP), (FY18: USD1,434 per ton DDP.

Sales of ferromanganese on a per-region basis for the current and previous financial years are illustrated as follows:

| Sale of ferromanganese ore on a per-region basis (%) | |

|

|

FY19 saw several major ferroalloy producers announce production cuts in an attempt to curb losses and accelerate the clearing of the over-supplied ferroalloy market. The uncertain economic environment continued to affect alloy demand in the markets outside China, with elevated input costs and weak alloy prices placing pressure on profit margins which are not expected to recover in the short term. Accordingly, by way of using a discounted cash flow model, management at Sakura have recorded an impairment charge against its property, plant and equipment of Malaysian ringgit (MYR) 338 million, of which Assmang's equity-accounted portion (54,36%) amounted to R625 million. In addition, management at Assmang assessed Assmang's equity-accounted carrying value of its investment in Sakura, by comparison to its determined fair value (less cost to sell) and an additional impairment charge in this respect of R388 million was recorded in this respect. The group's 50% share of the sum of these charges amounted to R507 million.

These impairment charges resulted in an overall decrease of 9% in the attributable profit of the Manganese division.

The Manganese division's capital expenditure increased by 77% to R2,3 billion (FY18: R1,3 billion), mainly due to R662 million capital spent on the modernisation and optimisation of Gloria Mine as well as a new slimes dam and thickeners for water recovery at the Nchwaning operations. At the end of FY19, approximately 93% of the approved capital of R6,9 billion on the Black Rock Expansion Project was committed or spent and 25% of the approved capital of R2,7 billion for the Gloria Mine modernisation and optimisation was spent.

Chrome

The attributable profit for FY19 decreased by 41% to R516 million (FY18: R875 million), due to lower prices for chrome ore and increased operating costs. The reduced profit was compounded by a labour strike suffered by Dwarsrivier in March 2019, which led to a decrease of 4% in production volumes. The cost management performance was disappointing, with unit production costs increasing by 14% over FY18.

The US-China trade conflict and subsequent trade actions had a negative impact on consumer confidence and resulted in lower than expected demand for stainless steel. The production of stainless steel in China increased by 3,4% from 25,6 million tons in the 2017 calendar year (CY17) to 26,6 million tons in CY18 and world stainless steel production increased by 5,4% in the same period. The over-supply of ferrochrome in the group's main market resulted in a decrease in demand for chrome ore, especially during the last quarter of FY19, which saw the average index market price for FY19 decreasing to USD187 per ton from USD224 in FY18 (44% chrome content material, delivered in China).

The weaker ZAR/USD exchange rate partially negated the decrease in prices, with revenue decreasing by 4% to R3,6 billion. The mine spent capital of R480 million, mostly on ongoing projects aimed at increasing plant efficiency.

Sales of ores on a per-region basis for the current and previous financial years are illustrated as follows:

| Sale of chrome ore on a per-region basis (%) | |

|

|

Wonderstone

The group has been mining pyrophyllite since 1937 from a deposit outside Ottosdal, approximately 300 kilometres south-west of Johannesburg, which it trades as Wonderstone. It is volcanic in origin and displays unique heat holding, insulation and pressure-resistant properties. The bulk of the material mined is beneficiated and reworked into components for export to the USA, the United Kingdom and the Far East. These components are utilised in various high-tech industrial applications, including the manufacture of synthetic diamonds and consumable products for the welding and electronics industries, and are sold as specialist ceramic products. The most significant market for Wonderstone products is its use in the manufacture of polycrystalline diamond (PCD) cutters for drilling in the oil and gas well industries.

The export market, being the most significant market for Wonderstone, had a slow start to the year but saw some business returning in the last half of FY19. The weakened exchange rate made up for some of the lost export sales volume. Local demand for manufactured products showed good growth, following the successful completion of a locally developed product. Demand for Wonderstone run-of-mine (ROM) material into China remained strong.

The attributable loss recorded by the Wonderstone operations amounted to R3,7 million (FY18: R1,4 million profit).

Group Line Projects

Demand in the wear lining market continued to be weak with very few major construction projects. Despite a revised marketing effort and cost cutting measures being implemented, the company could not produce a profit, but was able to contain losses to R3,6 million (FY18: R14,9 million loss). Following a strategic review of the business, a decision was made to divest from Wonderstone's shareholding in Group Line Projects and subsequent to year-end, on 14 August 2019, the group sold its shareholding in Group Line Projects for R6 million.

Marketing and shipping

Wholly owned subsidiary Ore & Metal Company Limited is responsible for the marketing and shipping of all the group's products, including those produced by Assmang. Strong relationships have been established with customers in the Far East, Europe, North America, South America, Africa and India, and products with a market value of approximately R35,6 billion (2018: R27,5 billion), on which it earns commission, were marketed and distributed in these regions during the year. The company is an established supplier to steel and allied industries worldwide and has operated effectively in these markets for over 80 years. Attributable profit after taxation for the year improved to R611,6 million (FY18: R409,8 million), due mainly to the weaker exchange rate, higher prices for iron ore, and the elevated but steadily declining manganese ore prices.

Minerais U.S. LLC

The group holds a 51% share in Minerais U.S. LLC (Minerais), which is a limited liability company registered in the state of New Jersey in the United States. Minerais is responsible for marketing and sales administration of the group's products in these countries, in particular manganese alloys, and it trades in other commodities related to the steelmaking industry. Minerais' contribution to the group's attributable profit for the year decreased to R29,8 million (FY18: R65,3 million) as a result of significantly reduced trading opportunities and a much greater reliance on commission income from its distribution businesses.

Technical and operational management

As technical adviser to Assmang and other group companies, African Mining and Trust Company Limited provides operational management services to the group's mines and plants. For these services it receives fee income, which is related to turnover in Assmang and to services provided to Dwarsrivier. The impact of increased commissions received of R146 million resulted in its attributable net profit after taxation for the year increasing to R254,9 million (FY18: R164,4 million).

Investments

Assore holds a 31,12% interest in IronRidge Resources Limited (IronRidge), which is accounted for using the equity method (refer to note 5 to the consolidated annual financial statements for more detail). IronRidge has a portfolio of gold, lithium, bauxite, titanium and iron ore prospects in Africa and Australia. During the financial year, IronRidge focused on its gold and especially its lithium exploration portfolio in the Ivory Coast and Ghana. The market value of the group's investment in IronRidge has decreased from GBP22,8 million (R410,4 million) at 30 June 2018 to GBP14,9 million (R267 million) at 30 June 2019.

The group holds a limited portfolio of listed shares which are selected and held in accordance with long-term investment criteria. In accordance with IFRS, the portfolio is valued in the financial statements at fair value. At 30 June 2019, the market value of the remainder of the portfolio was R317,8 million, based on a cost of R157,8 million.

Other income for the group includes interest received of R557 million (2018: R502 million) generated on cash in excess of current requirements, which was invested on a short-term basis in the money market, both on variable and fixed rates. The increased amount of interest received is mostly due to elevated average available cash balances and higher rates of interest, which prevailed in part due to fixed rates being higher than the variable rates.

Outlook

Global economic growth is being affected by increasing geopolitical risk. The uncertainties that prevail in the world markets may hamper steel demand in the year ahead which could have a negative impact on the prices we receive for our products. In response to the trade war initiated by the United States, China has increased its fiscal and monetary stimulus, announcing a new round of major infrastructure projects and various tax cuts. These actions, if successful in maintaining continued growth in China, should support demand for the group's products in the near term. The direction of prices will ultimately be determined by the level of discipline exercised by suppliers.

The mining industry in South Africa continues to face a high level of regulatory uncertainty and increased expectations from its various stakeholders. When combined with continued increases in electricity prices and wage demands that continually exceed inflation, significant pressure is being placed on the competitiveness of South African suppliers of commodities to world markets.

Appreciation

I would like to express my sincere appreciation to the group's customers and partners for their support during the year which made these results possible. I would also like to thank my executive team, the management teams at our operations, our dedicated sales and marketing colleagues around the world and all the staff of the Assore group for their support and tremendous contribution to this successful year.

Charles Walters

Chief executive officer

18 October 2019